512 South Mangum Street, Suite 100, Durham, NC, United States of America, 27701

Feeds

Avalara Simplifies Ever-Changing License, Product Registration, and Tax Requirements for Wineries

Sales tax compliance for beverage alcohol comes with its own set of rules. Avalara for Beverage Alcohol doesn’t just give you the latest tax rates, it helps you stay up to date on licensing and product registrations while integrating with other beverage alcohol industry tools.

Avalara helps businesses of all sizes get tax compliance right. In partnership with leading ERP, accounting, ecommerce, and other financial management system providers, Avalara delivers automated, cloud-based compliance solutions for transaction tax, including sales and use, VAT, GST, excise, communications, lodging, and other indirect tax types. Headquartered in Seattle, Avalara has offices across the U.S. and around the world in Canada, the U.K., Belgium, Brazil, and India. You can find more helpful information at avalara.com.

Visit Avalara at the WIN Expo on December 5, 2024 at booth 520

Register with the promo code: 520AVA to get a free tradeshow floor pass.

Conquering the Challenges of California Winery Property Tax Compliance

California produces more than 80% of U.S. wine and is home to some of the largest wineries in the country. Tax compliance can be complicated when your business involves managing multiple vineyards, operating specialized equipment, and even moving grape bins with forklifts. In addition to complying with beverage alcohol tax laws regulating shipping and selling wine, California wineries must also consider managing property tax compliance.

A typical California winery is responsible for paying property tax on real estate and personal property used in its business. Not complying with tax liabilities can leave you with the taste of sour grapes in the form of penalties.

In this post, we break down California property tax compliance for wineries to help you understand your tax liability and stay in good standing with tax authorities.

Taxing the vine: Real property tax compliance for wineries

Real property includes vineyards, winery buildings, and tasting rooms. County assessors consider multiple factors to come up with your real property assessment. When valuing vineyards, for example, they generally consider the number of acres, improvements like trellises and irrigation, and the vines themselves. It’s worth pointing out that under California law, new and replanted vines are exempt from property taxes for the first three years because they aren’t considered in full production.

The assessor typically has all the information they need to determine the assessed value of your real property and generally won’t require you to file a special form. An exception might be if you have a special assessment and must file agricultural exemptions. In this way, real property tax compliance is relatively straightforward for winery owners compared to personal property tax compliance. However, it’s not uncommon for larger wineries to owe tax to multiple jurisdictions because they have property in different locations. Staying on top of your property tax obligations for your California real estate can still be time-consuming.

It’s possible to overpay California property tax if the assessor doesn’t have accurate records about your real property, such as vineyards. According to the Napa County Assessor’s Department, only 60% to 65% of the vineyard owners who receive vine reports in any given year return them. “Failure to report timely can mean vines and [improvements] that have been removed may be assessed for several years after removal,” warns the department.

When it’s personal: Two types of California personal property tax statements for wineries

Wineries use specialized equipment for harvesting grapes at each stage of wine production, including crushing, fermentation, and bottling. Machinery used for winemaking is often defined as tangible personal property, which means the “movable” property, unlike a building. Tangible personal property is generally subject to property tax unless considered exempt under law, as can sometimes be the case for equipment used in agriculture.

Computers and furniture used at the winery and tasting rooms are also considered personal property and are usually taxable.

To stay compliant, your California winery must file annual property tax returns with the county assessor’s office in the jurisdiction where your personal property is legally located. In California, that means filling out either a Business Property Statement (Form 571L) or an Agricultural Property Statement (Form 571A). The forms ask for similar information but are not interchangeable, so submitting the right one is important. In addition, you can’t file the same form in multiple jurisdictions; each county has its own version. Unlike some other tax forms that can be submitted electronically, you’ll likely have to apply a stamp and send your return through the mail.

Getting a fair deal: Detailed records are key to an accurate personal property tax assessment

Both Forms 571L and 571A require you to provide details about your personal property that the county assessor will use to estimate the fair market value of your personal property. To determine normal or actual depreciation, the assessor generally will consider how much you originally acquired the asset for, how much it would cost to replace the asset, and the age of the asset.

You must maintain good purchase and maintenance records to ensure a fair assessment. If your mechanical and accounting teams communicate regularly, you’ll have a better idea of the useful life of the equipment that can serve as a reference for depreciation schedules.

If, for example, a forklift won’t run and you don’t properly report that on your return, it’s possible to overpay property tax. If a wildfire damages your crop and prevents your business from having a good year, that can lead to a decline in the value of your assets, known as obsolescence.

Again, if you don’t accurately document these factors, your assessment could be higher than it should be. If that happens, you have limited time to appeal the assessor’s valuation and provide further information. California property tax appeal deadlines vary, so make sure you know each county’s filing deadline.

Beyond property tax: Meeting your beverage alcohol tax obligations

So far, we’ve focused on property tax compliance for California wineries. But your business must also consider how you’ll handle California wine tax regulations and other aspects of beverage alcohol tax compliance. For many wineries, this is a challenge.

Staying on top of licensing and product registration requirements requires expertise.

Adhering to rules for age verification, volume limits, and dry area restrictions for direct-to-consumer shipments can be difficult, but it’s all necessary to stay in good standing with authorities.

Managing exemption certificates and filing returns for sales tax, excise tax, markup tax, and shipment reports is often time-consuming and complex, especially if your winery sells into multiple states.

Starting January 1, 2024, the California Bottle Bill will apply to containers containing wine. Any business that holds a manufacturing license or a wine shipper permit with the California Department of Alcoholic Beverage Control (ABC) will have to pay a fee.

Your 100-point tax compliance helper: Join the wineries automating with Avalara

If the thought of trying to meet your tax obligations is making you shrivel up like a raisin in a heat wave, there’s an easier way. Many businesses choose to automate compliance for multiple winery tax types. Avalara Property Tax and Avalara for Beverage Alcohol can help your California winery save time and keep up with regulatory requirements so you can focus on selling cases to customers.

California Bottle Fee to Apply to Wine and Spirits in 2024

Many aluminum, glass, and plastic containers in California are subject to refundable container recycling fees under the California Beverage Container Recycling and Litter Reduction Act (aka, California Bottle Bill Act), but many aren’t. Whether the Bottle Bill applies to a container depends as much on what the container holds as what it’s made of. And starting January 1, 2024, the California Bottle Bill will apply to containers containing wine and distilled spirits.

Many aluminum, glass, and plastic containers in California are subject to refundable container recycling fees under the California Beverage Container Recycling and Litter Reduction Act (aka, California Bottle Bill Act), but many aren’t. Whether the Bottle Bill applies to a container depends as much on what the container holds as what it’s made of. And starting January 1, 2024, the California Bottle Bill will apply to containers containing wine and distilled spirits.

This is a big change, but fortunately, California has given wine and spirits producers a long runway: The California Bottle Bill Act was broadened to include wine and spirits containers with the enactment of Senate Bill 1013 in September 2022.

Senate Bill 353, which was signed into law in October 2023, further clarifies certain requirements.

Read on to learn more about updates to the California Bottle Bill and how they’ll impact direct wine shippers, other wine and spirits manufacturers and distributors, and consumers in the state.

What is the Bottle Bill?

The Bottle Bill imposes redeemable recycling fees on aluminum, bimetal, glass, and plastic beverage containers. The revenue is used to fund the California Beverage Container Recycling Program (BCRP), subsidize recycling businesses, and expand demand for the recycled materials.

By allowing consumers to collect a California Refund Value (CRV) when they bring qualifying containers to certified recycling containers, the program also encourages Californians to recycle. California is working to achieve an 80% recycling rate for all aluminum, bimetal, glass, and plastic containers sold in the state.

Which beverage containers are subject to the Bottle Bill?

Through December 31, 2023, California’s Bottle Bill applies to aluminum, bimetal, glass, and plastic containers for the following beverages:

- All nonalcoholic beverages, except milk and vegetable juices over 16 ounces

- Carbonated fruit drinks, soft drinks, or water

- Noncarbonated fruit drinks, soft drinks, or water

- Coffee and tea beverages

- 100% fruit juice (less than 46 ounces)

- 100% vegetable juice (16 ounces or less)

- Beer and malt beverages

- Wine coolers and distilled spirits coolers

Starting January 1, 2024, the Bottle Bill also applies to containers for:

- Distilled spirits in all containers, including bladders, boxes, and pouches (all sizes)

- Wine in all containers, including bladders, boxes, and pouches (all sizes)

- 100% fruit juice (46 ounces or greater)

- 100% vegetable juice (greater than 16 ounces)

Refillable containers are exempt from the Bottle Bill.

Which containers are not included in the Bottle Bill?

The California Bottle Bill does not apply to containers for the following products:

- Food and nonbeverage containers

- Infant formula

- Medical food

- Milk

Who pays the Bottle Bill fees?

Manufacturers and distributors of beverages covered by the Bottle Bill are responsible for paying the applicable fees. Thus, they must register with the California Department of Resources Recycling and Recovery (CalRecycle) as a manufacturer, a distributor, or both a manufacturer and a distributor.

The Bottle Bill actually imposes two separate fees. Businesses registered as a manufacturer are responsible for paying processing fees. Businesses registered as a distributor are responsible for paying the California Redemption Value, or CRV. California allows distributors to claim a 1.5% administrative fee discount.

What is a beverage manufacturer?

When it comes to responsibility for paying the processing fee, a beverage manufacturer is anyone who:

- Bottles, cans, or otherwise fills beverage containers in California with a beverage that’s not beer, wine, or distilled spirits; or

- Holds a manufacturing license with the California Department of Alcoholic Beverage Control (ABC) for beer, wine, or distilled spirits, regardless of who fills the container; or

- Imports beverages into California for sale to consumers, dealers, or distributors; or

- Holds a certificate of compliance for beer or malt beverages with the ABC; or

- Holds a wine direct shipper permit with the ABC.

In October 2023, California updated the definition of a “beverage manufacturer” for wine, beer, and spirits to better align with industry standards and clarify that the holder of the ABC manufacturing license is liable for the bottle processing fee even if a third party bottles or otherwise fills the beverage container — so long as the licensee sells the product. If a third-party bottler fills and sells a product, the manufacturer would be considered responsible for the processing fee.

Processing fees and payments are subject to change. Current and historical processing fees and payments are available at CalRecycle.

What is a beverage distributor?

With respect to the California Redemption Value (CRV) fee, a distributor is:

- Any person who engages in the sale or import of qualifying beverages in qualifying beverage containers to a dealer in the state; or

- Any manufacturer or importer who engages in sales to consumers or dealers in California; or

- The person or entity named on the direct shipper permit issued by the ABC.

In October 2023, California passed a law that exempts a beverage distributor from the requirement to pay a redemption payment (CRV) for a beverage container used solely to pour wine, beer, or distilled spirits at a licensed wine, beer, or distilled spirits tasing room. It also exempts licensed beer tasting rooms from the definition of a dealer. This change takes effect January 1, 2024.

Does the bottle fee apply to direct shipments from out of state?

The Bottle Bill applies to direct shipments originating inside or outside California.

Per the law, “with respect to the payment of redemption payments for beverages manufactured outside the state and sold directly to consumers within the state with a direct shipper permit, the distributor shall be deemed to be the person or entity named on the direct shipper permit … and shall be responsible for paying to the department the total redemption payment for all sales and transfers made directly to consumers” in California.

Bottle Bill registration requirements for wine direct shipper permittees

Direct wine shipper permittees must register with CalRecycle and comply with all applicable requirements, including reporting and paying the processing fees and CRV fees imposed on beverage manufacturers and distributors by the California Beverage Container Recycling and Litter Reduction Act, respectively.

Businesses operating under one federal tax identification number need only submit one registration application, even if they sell multiple brands under that number. Businesses that have a separate federal tax ID for each brand or label will need to submit an application for each FEIN. In both cases, CalRecycle will decide if the applicant(s) is a manufacturer, a distributor, or both. CalRecycle could assign each FEIN a manufacturer account and distributor account.

Penalties for noncompliance

California takes recycling seriously. Should a direct wine shipper permit holder fail to register for and pay the redemption fee, it could have its wine direct shipper permit suspended or revoked by the Department of Alcoholic Beverage Control (ABC).

How much are the Bottle Bill fees?

The processing fee rates and California Refund Value (CRV) rates vary depending on the size of the container and the state’s recycling rate.

CRV rates are currently:

- 5 cents for a container with a capacity of less than 24 fluid ounces

- 10 cents for a container with a capacity of 24 fluid ounces or more (e.g., 750 ml wine bottles)

- 25 cents for a bladder, box, pouch, or similar container of wine and distilled spirits (starting January 1, 2024)

- 1.5% administrative fee

Processing fee rates are currently:

- None for aluminum

- $0.00375 for glass

- $0.00066 for #1 - PET (Polyethylene Terephthalate)

- $0.00602 for #2 - HDPE (High Density Polyethylene)

- $0.05014 for #3 – PVC (Polyvinyl Chloride)

- $0.01696 for #4 – LDPE (Low Density Polyethylene)

- $0.05573 for #5 - PP (Polypropylene)

- $0.00348 for #6 - PS (Polystyrene)

- $0.13610 for #7 - Other

- $0.04799 for Bimetal

CalRecycle keeps a complete list of current and historical processing fee rates and CRV rates.

Are there any Bottle Bill labeling requirements?

There are labeling requirements for beverages subject to the Bottle Bill.

Eligible containers containing qualifying beverages need to have one of the following California Redemption Value (CRV) messages on the label:

- California Redemption Value

- CA Redemption Value

- California Cash Refund

- CA CRV

- CA Cash Refund

However, beverage manufacturers have until July 1, 2025, to add the CRV message to the labels of the following products:

- Distilled spirits

- Wine and distilled spirit coolers with greater than 7% ABV

- Wine (including wine from which alcohol has been completely or partially removed, whether sparkling or carbonated)

- Wine or distilled spirits in a box, bladder, pouch, or similar container

- 100% fruit juice (46 ounces and greater)

- 100% vegetable juice (greater than 16 ounces)

The following beverages are exempt from CRV labeling requirements:

- Distilled spirits, wine, and wine and distilled spirit coolers with more than 7% ABV that are filled and labeled before January 1, 2024

- 100% fruit juice (46 ounces and greater) and 100% vegetable juice (greater than 16 ounces) that are filled and labeled before July 1, 2024

How does California's Bottle Bill raise money?

Beverage manufacturers and distributors make processing fee and/or CRV payments on eligible bottles (as required) to CalRecycle, which deposits the collections in the California Beverage Container Recycling Fund.

Consumers receive a California Refund Value (CRV) payment from the fund when they return eligible containers to a certified recycling center.

Since not every qualifying container is returned for its CRV, CalRecycle collects more revenue from distributors than it pays to consumers. Leftover revenue from unredeemed containers helps fund “other recycling-related activities,” such as administrative costs, hauling fee payments, and recycling grants to various entities.

States with bottle bills

California isn’t the only state with a bottle bill. According to the National Conference of State Legislatures, 10 states and one territory had bottle bills as of March 2020:

- California

- Connecticut

- Hawaii

- Iowa

- Maine

- Massachusetts

- Michigan

- New York

- Oregon

- Vermont

- Guam

Each state’s policy is different, and rates range from about two cents to 15 cents per bottle, depending on the container and what it holds. Iowa and Maine include wine containers but provide an exemption for wine sold under a DTC permit.

States periodically consider new or expanded bottle bills. One of the next big changes on the horizon is that wine in a can will be subject to Oregon’s Bottle Bill starting July 1, 2025.

Want to learn more about beverage alcohol tax compliance? Connect with us.

The Mixed-Up Classification and Taxation of RTDs

Ready-to-drink beverages are having a heyday in the United States. The ready-to-drink (RTD) category grew more than any other spirits category in 2022, and the RTD category value is expected to reach $11.6 billion through 2026. Such strong sales are causing some states to reconsider how to best classify — and tax — RTDs. When it comes to defining and taxing ready-to-drink beverages, there’s little if any consistency from state to state.

What is an RTD?

What is an RTD?

As the name suggests, an RTD is a beverage manufactured and packaged for immediate, easy, individual consumption. While that may call cans of beer to mind, RTD typically refers to drinks assembled from two or more ingredients, like cocktails, that are sold in a manufacturer-sealed container. RTDs usually contain alcohol, though there are nonalcoholic varieties.

A margarita prepared by your favorite Mexican restaurant for off-premises consumption is not a ready-to-drink beverage. The premixed, canned Jack Daniel’s & Coca-Cola RTD that hit the U.S market in March 2023 is.

The Alcohol and Tobacco Tax and Trade Bureau (TTB) doesn’t define ready-to-drink beverages, and every state defines RTDs differently, if at all.

For instance, Arkansas defines a ready-to-drink product as “a product containing spirituous liquor with a final finished product of no greater than 15% alcohol by weight.” A “mixed spirit drink” in Michigan is made with distilled spirits and other ingredients, has an alcohol by volume (ABV) of no more than 13.5%, and is packaged in metal cans; if packaged in any other type of container, a mixed spirit drink may not exceed 10% ABV. In Nebraska, a ready-to-drink cocktail is a beverage or other confection containing spirits in an original package that contains 12.5% or less ABV.

RTDs are commonly categorized by manufacturing method or the base alcohol ingredient:

- Malt (partially germinated cereal grains like barley) or malt substitute (including sugar);

- Spirits (gin, rum, tequila, vodka, whiskey, grain neutral spirits); or

- Wine (fermented grapes or other fruits).

Ingredients matter because they’re tied to tax: States typically tax beer and other malt-based beverages differently than distilled spirits, and liquor differently than wine. Many states have taken a similar approach to taxing RTDs.

How are RTDs taxed?

To understand how RTDs are taxed, it helps to start with a primer on how state excise taxes apply to beer, wine, and spirits.

State taxes on beer, wine, and spirits are linked to alcohol content

Tax rates tend to be linked to alcohol content. With a higher alcohol content than beer or wine, distilled spirits are taxed more heavily than beer or wine. Malt beverages have relatively low alcohol by volume and are subject to the lowest tax rates. A happy medium (stronger than beer but weaker than spirits), wine is typically taxed somewhere between the two.

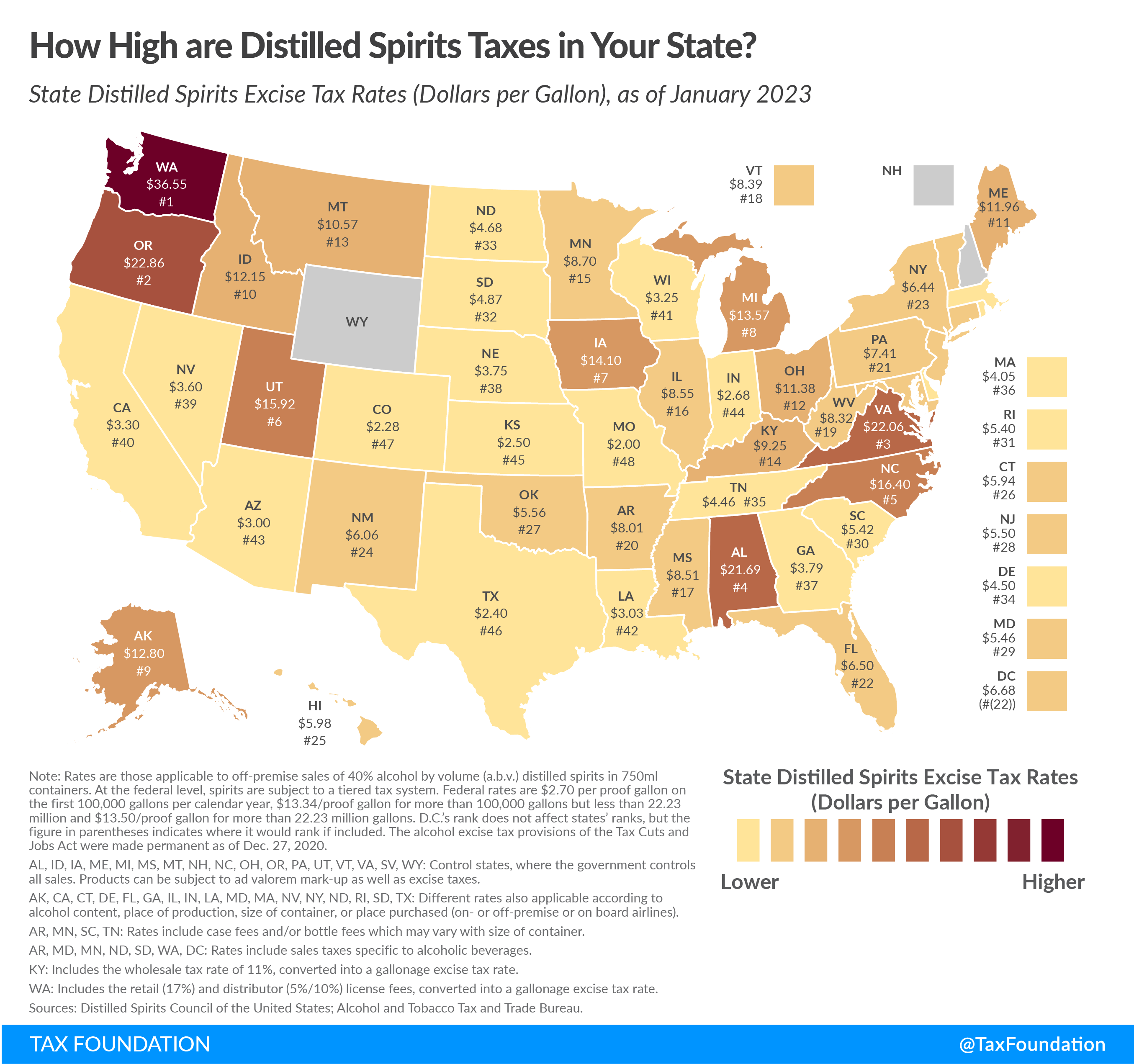

The following chart gives a taste of how different tax rates for alcoholic beverages can be from state to state (in dollars per gallon) — but just a taste. Beverage alcohol excise taxes are layered and complex, and the responsibility to pay them may fall on the manufacturer, retailer, or wholesaler, depending on the type of transaction.

| State | Beer | Wine | Spirits |

|---|---|---|---|

| California | $0.20 | $0.20 | $3.30 |

| Florida | $0.48 | $2.25 | $6.50 |

| Missouri | $0.06 | $0.42 | $2.00 |

| New York | $0.14 | $0.30 | $6.44 |

| Ohio | $0.18 | $0.32 | $11.38 |

| Texas | $0.19 | $0.20 | $2.40 |

| Utah | $0.41 | NA | $15.92 |

| Washington | $0.26 | $0.87 | $36.55 |

RTD taxes tend to mimic taxes on spirits, wine, and beer

It’s common for states to tax RTDs based on their main alcohol ingredient, so in many states, spirit-based RTDs are subject to a higher tax than their malt-based and wine-based counterparts.

In West Virginia, for instance, a spirit-based RTD with 6% alcohol by volume (ABV) is taxed 35 times more than a malt- or sugar-based RTD with the same alcohol content. “The rate for malt- and sugar-based beverages with a 6% ABV is $0.02 per 12-ounce can,” according to the Distilled Spirits Council of the United States, “versus $0.71 per 12-ounce can of a spirits-based beverage.”

That’s not the case in every state. A February 2023 Ready-to-Drink Alcohol Tax Report by the Maryland Alcohol and Tobacco Commission notes that 25 states have a “Low Spirit” tax rate in addition to a “Full Spirit” tax rate. The lower tax rate applies to spirits with 24% or less ABV in New York but 6% or less ABV in Alabama. See the map below for more state-specific details.

Most of these states didn’t create the low-spirit rate with RTDs in mind. The low rate may apply to RTDs — but may not.

At least 12 states attempted to establish lower tax rates for “low-proof” spirit-based RTD beverages in 2021 and 2022: Alabama, Arizona, Hawaii, Kentucky, Maryland, Michigan, Minnesota, Nebraska, North Carolina, Vermont, Washington, and West Virginia. Only three states enacted the new laws:

Michigan SB144 (2021) reduced the excise tax rate for low-proof, spirit-based RTDs effective August 23, 2021.

Nebraska LB274 (2021) established a new tax rate for RTDs as of July 1, 2021. At $0.95 per gallon, the tax is significantly lower than the full spirits tax rate of $3.75 per gallon (though not as low as the $0.31 originally sought).

Vermont H730 (2022) lowered the rate and stipulated that RTDs not be sold through the state’s alcohol-controlled model. The new policy and tax rate took effect July 1, 2023.

Several states introduced legislation in 2023 to lower taxes on certain spirit-based RTDs and/or expand retail options for spirit-based RTDs, with little success. California SB-277 sought to allow more retailers to sell low-ABV spirit-based RTDs, but the bill stalled. A similar bill was left pending in committee in Texas, while a Pennsylvania bill was laid on the table.

IWSR Drinks Market Analysis expects industry advocates to continue to push for states to level the playing field by allowing spirit-based RTDs to be sold alongside their malt-based and wine-based counterparts. A more equitable tax policy could also help grow the spirit-based market. Even with existing policies, consumer taste for spirit-based RTDs is growing.

Consumption of ready-to-drink beverages grew more than 104% in the past two years, according to NielsenIQ, while the market for other alcoholic beverages contracted. If that rate of growth continues, it could encourage states to develop more consistent definitions for ready-to-drink beverages, and perhaps update their tax policies as well. If any do, we’ll let you know at the Avalara Tax Desk.

Avalara for Beverage Alcohol can help support your RTD tax compliance needs. Contact us to learn more.

Five Ways to Help Simplify Beverage Alcohol Taxes, Licenses, and Registrations

What Wineries Need to Know About Product Registrations

Whether your wine label is classy or clever matters more to your buyers than it does to authorities who deem your cabernet or chardonnay fit for sale. But your wine label is more than a marketing tool. You can’t sell beverage alcohol without first obtaining all required federal and state alcohol product registrations. And to successfully register your product, your label must be approved by the appropriate federal and state authorities.

Registering your wine at the federal level

As a producer, your first order of business is to make sure your label complies with regulations set by the U.S. Department of the Treasury Alcohol and Tobacco Tax and Trade Bureau (TTB).

Assuming your wine contains more than 7% alcohol by volume (ABV), as is typically the case, you’ll need to obtain a Certificate of Label Approval (COLA) to sell it into other states. If you only intend to sell in the state where your wine is bottled or your wine has an ABV below 7%, you can apply for an exemption.

In either case, you have to make sure certain mandatory information — like the wine’s designated class description and sometimes the appellation of origin — appears on the container. Here’s a fun fact: The label that faces the consumer in a retail display doesn’t necessarily have to contain all these details; what TTB considers the brand label may actually be what buyers read when they turn your bottle around. So as a producer, you need to know what information can go where.

In some cases, TTB must approve your wine’s formula (your special recipe) before you can apply for a COLA. This is often the case if flavors or colors are added. Let’s say you make a blended fruit wine from raspberries and cherries. Depending on whether you ferment the juices at the same time, add juice as a flavor after fermentation, or mix two finished wines, you may or may not require formula approval. If required, you’ll need to provide a complete list of ingredients, a step-by-step description of how your product is made, and potentially a sample for lab analysis.

Navigating state alcohol product registration requirements

That’s just the federal level. You also have to register your product with state authorities where your winery is located and where you plan to sell. Unfortunately, it’s not as simple as submitting the same form to each state where you want to do business. Not all jurisdictions require product registrations and those that do have different requirements. Let’s take a look at a few examples:

Want to sell your wine in Illinois? You’ll have to submit your application to the Illinois Liquor Control Commission. Products that are registered and approved for direct shipment to consumers must be resubmitted for approval for wholesale distribution.

Labels approved for wholesale distribution in Connecticut are also approved for direct-to-consumer (DTC) sales. To sell your wine in the Constitution State, you’ll have to submit a color copy of each label, evidence of federal label approval, and independent lab analysis or a notarized statement detailing the alcohol type and proof with your product registration application. You’ll also need to provide the Connecticut Department of Consumer Protection Liquor Control Division with your wholesaler appointment letter.

Selling in Louisiana requires electronically registering each COLA with the Louisiana Office of Alcohol and Tobacco Control — a paper filing option isn’t available. If you register your label for distribution to a local wholesaler in the state, you can’t also register it for DTC sales. However, any label sold to a Louisiana wholesaler may be shipped directly to a consumer in the state who purchased the wine on-site.

Product registration and renewal fees vary widely. They can be nominal or even free to as much as $200 per product or more in some states.

States often vary in how they determine what the product registration fee is associated with. Some states charge per brand. In others, you must register each product/label. Some states even connect fees with product class and alcohol content. For example, the Oklahoma Alcoholic Beverage Laws Enforcement Commission groups domestic wine by brand within three categories: under 14% ABV, 14% ABV or greater, and sparkling. However, for foreign wines, they group by country of origin within those three categories; brand is irrelevant.

Rules aren’t static. States frequently create new regulations or revise existing ones. Understanding the latest requirements can be difficult but it’s necessary to remain in good standing with authorities.

Keeping up with product registration renewals and label revisions

It’s not enough to submit all the paperwork once. Many states require you to renew your production registrations every three years or annually to stay compliant. Staying on top of deadlines can be challenging but it’s important to avoid penalties. Some states require you to renew in June, others in December, Tennessee has a May 31 deadline, and others base the deadline on when you submitted your application.

Wine isn’t like other consumer packaged goods. Unlike a box of cereal or a six-pack of soda, wine changes every vintage. Any changes you make to your product or label may or may not require you to reregister with the TTB and/or state. TTB has expanded the list of label changes that can be made without approval, but even if you don’t need a new COLA, you may still need the official thumbs-up from states where you sell, and that can require additional paperwork.

Automating product registrations to make compliance easier

If keeping track of your product registrations seems like too much to handle on top of everything else you do, Avalara Product Registration for Beverage Alcohol can help. The solution automates product registrations, renewals, and revision requests so you can focus on other revenue-generating tasks and have time left over to pop the cork on your favorite bottle.

Five Ways to Help Simplify Beverage Alcohol Taxes, Licenses, and Registrations

Event Type: Webinar

Event Date: 10/19/2023

Winemaking is a labor of love; tax compliance on the other hand … not so much. Maintaining beverage alcohol compliance is complicated and time-consuming because of constant changes in rules and regulations.

Join this webinar to learn:

- How to get licensed where you sell by automating your license renewals

- How to register your products and keep up with various state and federal requirements

- How to calculate the correct tax for your products

- How to properly maintain compliance with direct-to-consumer (DTC) shipping

- How to simplify processes and improve accuracy while filing tax returns

Speakers

Sarah Faria – Director, Tax Compliance Services

Sarah Faria – Director, Tax Compliance Services  Shannon Fahey – Tax Research Analyst II

Shannon Fahey – Tax Research Analyst II

Five Beverage Alcohol Industry Changes Causing Tax Compliance Challenges

Tennessee Thumps Online Liquor Stores with 21st Amendment Act

Only a handful of states allow direct-to-consumer (DTC) shipments of spirits, and Tennessee isn’t one of them. But apparently that hasn’t prevented some businesses from selling and shipping spirits directly to consumers in Tennessee.

Only a handful of states allow direct-to-consumer (DTC) shipments of spirits, and Tennessee isn’t one of them. But apparently that hasn’t prevented some businesses from selling and shipping spirits directly to consumers in Tennessee.

During separate investigations, undercover agents from the Tennessee Alcoholic Beverage Commission (TABC) purchased and received unauthenticated and untaxed distilled spirits from six different online retailers, according to a press release issued by Tennessee Attorney General and Reporter Jonathan Skrmetti. One special agent purchased a 750-milliliter bottle of Evan Williams Peach Whiskey from an online seller and had it delivered to a Tennessee address. Another special agent purchased 12 50-milliliter bottles of Sheep Dog Peanut Butter Whiskey from a different online seller and had it delivered to a Tennessee address. And so on.

None of the retailers have a license to ship spiritous liquors directly to consumers from outside the state, because there is no such license in Tennessee.

The TABC sent cease-and-desist letters by certified mail to each of the retailers. One such letter explained, “As a retailer, you are not eligible for a Winery Direct Shipper License, and thus any shipping of wine or other alcoholic beverages by you to consumers in the State of Tennessee is illegal.” Approximately 10 months after sending that letter, a TABC special agent purchased vodka from the retailer’s website and had it shipped to a Tennessee address.

In fact, after receiving the cease-and-desist letter, “each company continued to ship distilled spirits to Tennessee illegally,” according to the Attorney General and Reporter. And so, on July 14, 2023, the Attorney General and Reporter filed a federal lawsuit “to immediately stop the flow of illegal liquor shipments facilitated by six unlicensed out-of-state defendants” on the grounds that “the defendants unlawfully facilitated shipments of distilled spirits for which no state license is available.”

This isn’t the first time Tennessee has cracked down on illegal DTC shipments of alcohol, but it is the first time a Tennessee Attorney General is prosecuting a violation of law under the 21st Amendment Enforcement Act. If successful, it likely won’t be the last. The 21st Amendment Enforcement Act allows state attorneys general to seek injunctive relief against anyone believed to be illegally importing or transporting alcohol within a state.

Out-of-state businesses that may be selling distilled spirits online and shipping to Tennessee should take note.

Russell Thomas, Executive Director of the TABC, said he was happy Attorney General and Reporter Skrmetti decided to prosecute this case. “Our agents and staff worked hard to collect the evidence against these bad actors,” he said. “Too often, we find websites operated by unscrupulous individuals willing to deceive consumers.” The Law Enforcement section of the TABC consists of 38 special agents whose primary responsibility is to enforce the state’s liquor laws.

Who is at fault? The retailer, or the consumer?

Both may be at fault under Tennessee law: “It is an offense for any person, firm, corporation, or association to import, ship, deliver, or cause to be imported, shipped, or delivered into this state any alcoholic beverages upon which the tax imposed by this title has not been paid or where such transportation is not authorized under this title to an entity possessing a license issued under this title. A violation of this subdivision (b)(1) is a Class E felony.”

Who pays the piper is another matter. Though Tennessee can go after individual consumers, it may get more bang for the buck by going after businesses that are illegally selling and shipping alcohol into the state.

State officials expect businesses to know the law and abide by it and may take them to court — literally — if they don’t. Interestingly, one retailer involved in the lawsuit states in its terms of service, “The buyer is solely responsible for the shipment of alcoholic beverage products … We make no representation relative to your right to import spirits or wine into your state. The buyer is responsible for the shipment of alcoholic products purchased and determining the legality and consequences of having spirits or wine shipped to them.”

Time will tell whether such a disclaimer holds any water with the courts.

Illegal liquor sales deprive the state of tax revenue

Tennessee has powerful motivation to prevent the illegal — and untaxed — direct shipments of liquor in the state: Such sales deprive the state of tax revenue.

“The State of Tennessee generates revenue through taxation of the retail sale of spirits and wine,” explains the legal complaint. “The illegal, unlicensed direct-to-consumer shipment of spirits causes a loss in tax revenue generated by the legal sale of spirits by licensed Tennessee retailers.” According to the Urban Institute, in 2020, Tennessee was the state with the highest share of general revenue from alcohol taxes.

The takeaway

The costs of noncompliance can be high.

The Tennessee Attorney General and Reporter is seeking:

- Preliminary and permanent injunctive relief under the 21st Amendment Enforcement Act and the Tennessee Consumer Protection Act (TCPA), prohibiting the defendants from continuing to violate Tennessee law

- The imposition of cumulative civil penalties against the defendants (the TCPA provides for a fine of up to $1,000 for each violation)

- Reimbursement of investigative expenses incurred

- Reimbursement for the costs and expenses of investigation and prosecution of actions under the TCPA, including attorneys’ fees

- Any other relief deemed appropriate

The Attorney General and Reporter is requesting a jury trial.

Learn more about beverage alcohol trends in our beverage alcohol tax changes report.

Five Beverage Alcohol Industry Changes Causing Tax Compliance Challenges

Event Type: Webinar

Event Date: 08/24/2023

Beverage alcohol businesses are encountering big challenges throughout 2023. In this round-up, Avalara will present some industry-pressing issues as part of their annual Bev Alc deep dive report.

Join this webinar to learn:

- How supply chain bottlenecks and climate change are front and center amongst major challenges in the industry putting the squeeze on materials and adapting to severe weather events

- How Direct-to-Consumer (DTC) shipping for beverage alcohol businesses has increased legislations

- How sustainability is playing a crucial part in the beverage alcohol industry moving to the top of the priority list

- How beverage alcohol producers may need to adapt to new labeling requirements down the road

- How states are trying to raise the tax rates on alcoholic beverages but lower the tax rates on others

All webinar attendees will receive a copy of the 2023 Avalara Tax Changes Beverage Alcohol Tax Compliance Report.

Webinar: August 24, 11am - 12pm PT

Speakers

Sarah Faria – Director, Tax Compliance Services Shannon Fahey – Tax Research Analyst II

{kind=link}

About

Avalara for Beverage Alcohol

Simplifying regulatory compliance for suppliers, distributors, and retailers in the beverage alcohol industry

We combine software and service to manage the complexities of compliance.

Avalara for Beverage Alcohol automatically calculates tax rates using the latest tax information, while working seamlessly with other Avalara products and beverage alcohol industry tools. We also obtain and renew licenses, register products at federal and state levels, and generate shipment reports and tax returns on your behalf.

Avalara AvaTax for Beverage Alcohol

Beverage alcohol industry regulations and tax rules exist at the federal, state, county, and city levels — with little or no consistency between jurisdictions. AvaTax for Beverage Alcohol helps reduce non-compliance and audit risk exposure.

Avalara Licensing for Beverage Alcohol

Failure to properly register and maintain state beverage alcohol licenses can result in revocation of licensure in the state, and potentially at the federal level. Licensing for Beverage Alcohol tracks registration with the Federal Alcohol and Tobacco Tax and Trade Bureau (TTB), state departments of revenue (DORs), and Alcohol Beverage Control departments (ABCs).

Avalara Product Registration for Beverage Alcohol

Secure the right permits in the right places and make sure every label is properly registered at the federal and state levels. With Product Registration for Beverage Alcohol, we’ll take care of the heavy lifting, so you can stay on top of this ongoing task.

Avalara Returns for Beverage Alcohol

Failure to comply with reporting requirements and tax remittance can put business licensure in jeopardy. With Returns for Beverage Alcohol we manage your end-to-end returns process for you, ensuring compliance while reducing manual effort.

Contact

Contact List

| Title | Name | Phone | Extension | |

|---|---|---|---|---|

| No contacts found | ||||

Location List

| Locations | Address | State | Country | Zip Code |

|---|---|---|---|---|

| Avalara | 512 South Mangum Street, Suite 100, Durham | NC | United States of America | 27701 |

List of Locations

Facebook feeds

Profile Picture